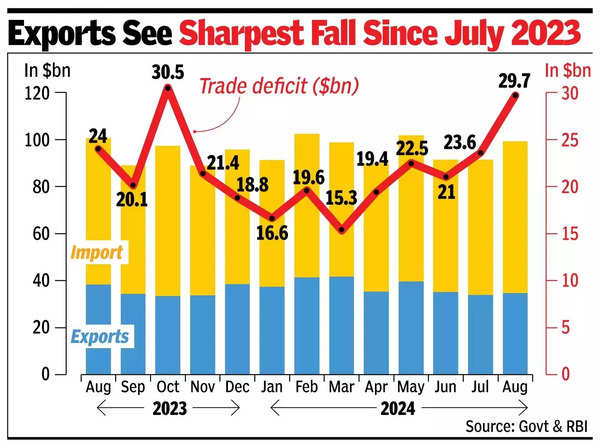

NEW DELHI: India’s trade deficit neared record level in Aug as a surge in gold shipments pushed up monthly imports by 3.4% to an all-time high of $64.4 billion, while exports fell 9.4% to $34.7 billion.

As gold imports more than doubled to a new high of over $10 billion, the commerce department on Tuesday said total imports rose to $64.36 billion in August, marginally higher than the previous record of $64.35 billion in June 2022.

Commerce secretary Sunil Barthwal attributed the increase to higher prices, a reduction in customs duty, stocking ahead of the festival season. The numbers indicate that some of the gold that was smuggled due to high tariffs are now coming via legal channels. As a result, the trade deficit widened to $29.7 billion, just a shade lower than the $30.4 billion gap between exports and imports recorded in last Oct.

“It is not a matter of concern for an emerging market economy. There is huge consumption demand coming from an economy that is growing at double the rate of the world economy. As exports grow and you join the global value chain, you have to import certain things to export. To the extent that there is foreign exchange (reserves), these are perfectly normal numbers,” Barthwal said.

He said that exports had dropped largely due to a fall in oil prices (resulting in lower value realisation for petrol and diesel) as well as due to low demand for gems and jewellery and rice exports being checked by govt. The fall in exports is the sharpest since July 2023, when it had shrunk 9.9%.

Lower crude oil prices meant that imports fell over 32% to $11 billion, while petroleum product exports were almost 38% lower at around $6 billion. “There is a huge challenge for exports in the current global situation… Despite the dark clouds globally, India is a bright spot,” Barthwal said.

Barthwal said several countries had seen a decline in imports, which was impacting exports and demand remained weak in the US and Europe, while China was in the midst of a slowdown. Fieo president Ashwani Kumar said trade disruptions – led by logistical challenges, such as lack of shipping space, irregular shipping schedule, ships skipping Indian ports – and declining commodity prices have hit exports.

Govt is drawing comfort from the services side, where exports rose 7% to $30.7 billion, while imports grew under 4% to $15.7 billion. “Tech-intensive sectors, including electronics, pharma, and engineering goods, continue to demonstrate resilience as key contributors to export growth. In terms of destinations, exports to non-traditional markets, such as Kenya and Brazil registered strong growth,” said India Exim Bank MD Deepali Agrawal.